Britain's 'missing billions' put UK on the back foot for Brexit

Jonathan Perraton, University of Sheffield

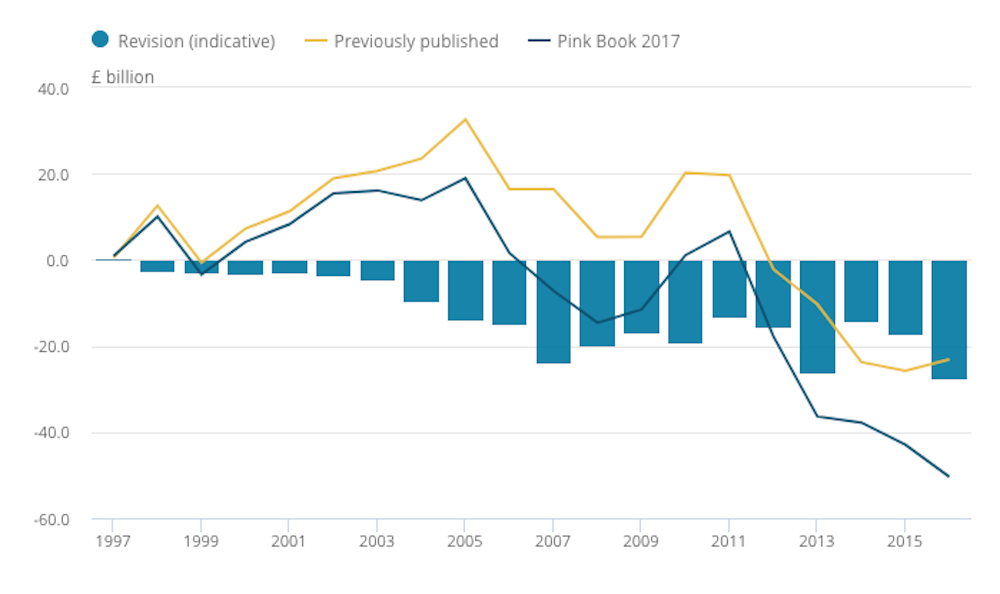

Britain has £490 billion less in its coffers than previously thought, according to revised estimates of Britain’s balance of payments from the UK’s official statistics body, the ONS. Whereas previous estimates indicated that in 2016 Britain’s assets overseas exceeded its liabilities to the tune of £469 billion, this has now been revised downwards to a net deficit of £22 billion. In the context of the potential disruption to trade and foreign investment from Brexit, this is a worrying development.

It is important to note that this does not mean that the country has suddenly become nearly half a trillion pounds poorer. The ONS has now collected more detailed data on Britain’s financial transactions with the rest of the world to build up a more accurate picture of its net stock of external wealth. Nevertheless, the figures do indicate that the UK’s external wealth position is much weaker than previously thought.

The country’s net international investment position represents the difference between UK residents’ holdings of assets overseas and foreigners’ holdings of assets in the UK. Although the ONS revision appears dramatic, it should be borne in mind that both British assets held overseas and foreign holdings of British assets are large, each totalling upwards of £10 trillion. Relative to these totals, the difference between these two figures is small.

Plus, this data comprises a range of assets, including British companies investing overseas and foreign companies investing in the UK, as well as cross-border holdings of company bonds, shares and other financial assets. Collecting data on this range of assets is a complex task and the ONS has widened and improved its data collection here. As a result, it has revised downwards its earlier estimates of Britons’ holdings of a range of foreign assets.

Cause for concern

The fall in the pound since the Brexit referendum result increases the sterling value of British assets held overseas. This has improved the external net asset position of the UK, but by substantially less than earlier estimates.

The UK has run a current account deficit continuously since the mid-1990s, reaching a peacetime record deficit relative to GDP in 2014. The longstanding deficit on trade in goods is partially offset by a surplus on trade in services; in most years before 2007, a net inflow of receipts from foreign investments also made a positive contribution.

If a country is running a deficit with the rest of the world on its current account then it must borrow from the rest of the world to finance this. Britain therefore has to attract funds from overseas. As Bank of England governor Mark Carney put it (channelling Blanche DuBois) the UK is reliant on the “kindness of strangers” to fund its external deficit. But borrowing from abroad weakens a country’s net international investment position over time, as external liabilities rise.

The detail of these figures raises several areas of concern. The fall in the pound since the referendum has only had a limited impact on improving the trade balance. Exports have risen, but only modestly. Flows of returns to foreigners’ investments in the UK have risen relative to returns received in Britain on British investments overseas.

Crucially, in terms of attracting investment in the future, the most recent figures indicate a decline in foreign direct investment inflows. More multinational companies are investing overseas relative to foreign companies investing in the UK. The figures also point to a sharp movement away from UK equities (company shares) by foreign investors.

Brexit challenge

It is best to not to leap to conclusions about the long term from the most recent statistics, but they do point to a weakening of the UK’s external position and the economy becoming less attractive to foreign investors. These figures point to major challenges in the context of Brexit.

Leaving the European Union is likely to hit Britain’s trading position, including in business and financial services where the UK runs a surplus with the rest of the EU. If Britain had a positive net international investment position, as previous estimates indicated, that would have provided some cushion as those investments would provide returns in the future. Instead the small negative position indicates that the total investments Britain has overseas are less than the value of foreign investments in the UK, such that returns on British investments overseas will be offset by the outflows from returns to foreign investments in the UK.

Jonathan Perraton, Senior Lecturer in Economics, University of Sheffield

This article was originally published on The Conversation. Read the original article.

Comments

Post a Comment